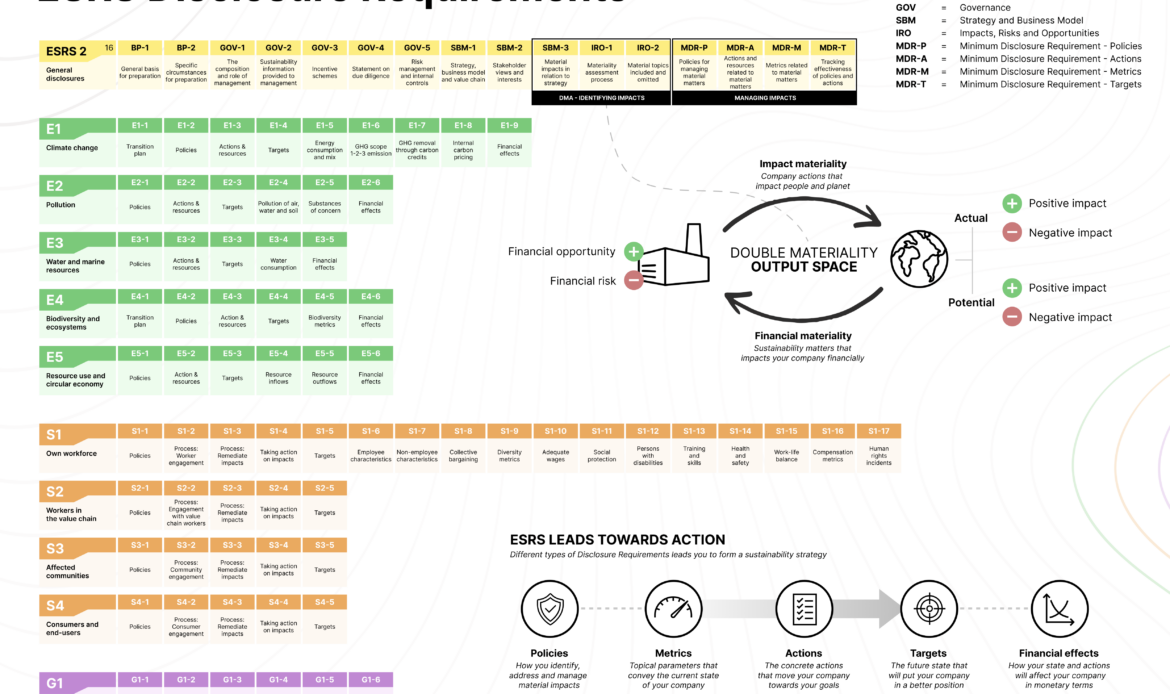

The ESRS Periodic Table – Great help for practitioners!

The ESRS Periodic Table offers an overview of ESRS requirements, highlighting the types of DRs, their interoperability, and the output space for the Double Materiality Assessment (DMA).

Effectively communicating the content of the ESRS standards and their depth in terms of Disclosure Requirements (DRs) is essential for CSRD practitioners as they support sustainability reporting and strategy implementation.

1.Topical Standards and Disclosure Requirements

Similar to a periodic table, each row (E1, E2, etc.) represents a specific topical standard, with its corresponding disclosure requirements (DRs) listed in the columns. This structure allows for quick identification of the number and types of DRs, such as Policies, Metrics, Actions, Targets, and Effects. Abbreviation keys are provided to simplify complex ESRS terminology, facilitating faster recognition and easier navigation through extensive ESRS requirements.

2. ESRS Leads Towards Action

ESRS goes beyond mere reporting; it guides practitioners through a strategic process that drives the company towards more sustainable operations. The “ESRS Leads Towards Action” flowchart illustrates how different types of DRs interact to create a strategic model for sustainability. The process begins with defining policies for topical areas where the company has, may have, or could have an impact. It continues with data collection to establish the company’s current state (Metrics), setting goals (Targets), planning initiatives (Actions), and ultimately assessing the potential outcomes (Financial effects).

3. Double Materiality Output Space (DMA)

The Double Materiality Assessment (DMA) process, as outlined in SBM-3, IRO-1, and IRO-2, involves a systematic examination of the company’s value chain and its components. Practitioners must evaluate both impact materiality and financial materiality, leading to six possible outputs. A visual representation of these outputs provides a clear overview, helping to avoid confusion between Positive/Negative impacts in terms of Actual/Potential scenarios, and financial perspectives where Positive/Negative is viewed as Opportunity and Risk. For impact materiality, practitioners assess whether an actual impact is positive or negative, while potential impacts also require an evaluation of the likelihood of occurrence. For financial materiality, practitioners must identify risks or opportunities and quantify them in monetary terms.